Whether you are a first-time buyer, a seasoned investor, or a professional evaluating a portfolio, understanding how property is priced in the UAE is one of the most important skills you can develop. The market here is unlike most others — it is driven by a combination of global capital flows, government policy, developer branding, and hyper-local supply dynamics. This guide breaks down the key factors that determine the value of a unit or villa, and how to approach a valuation with the rigour it deserves.

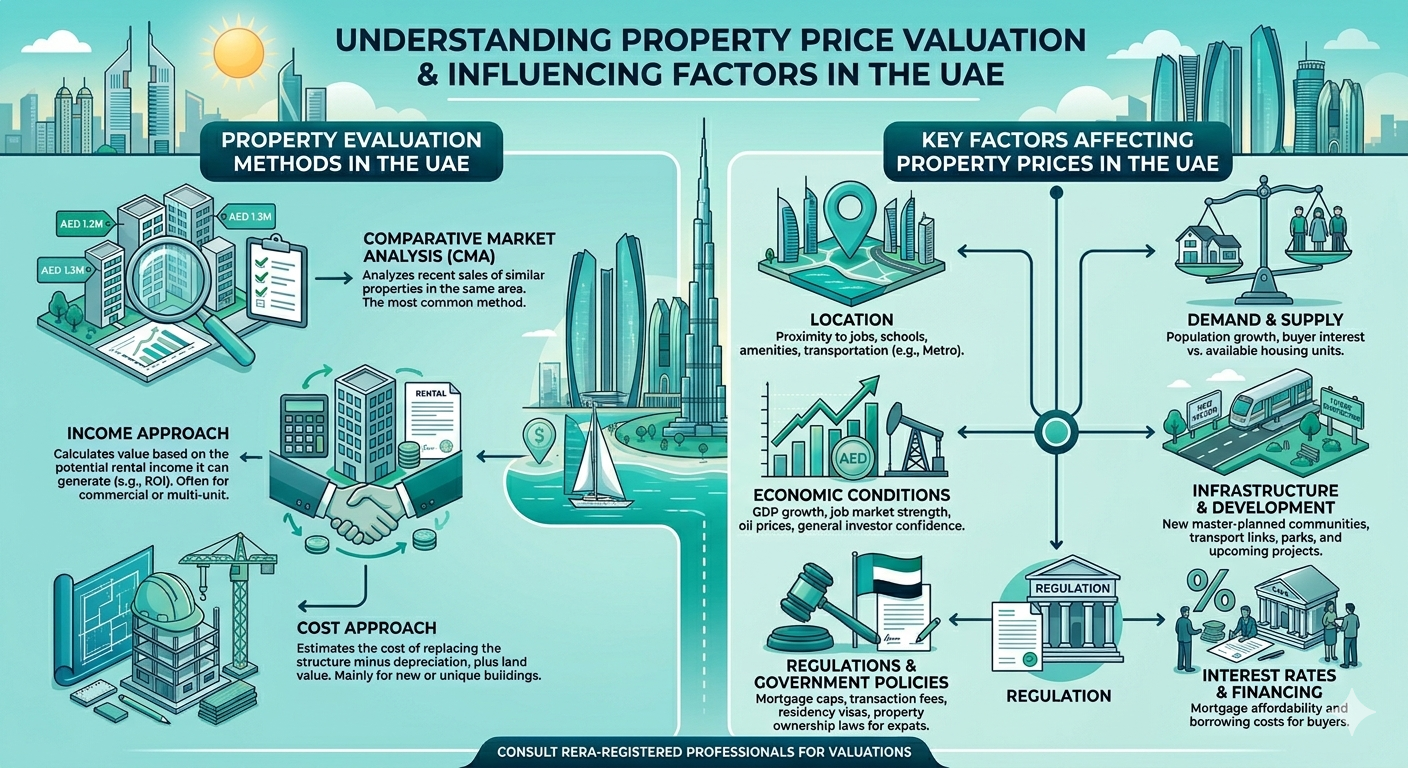

1. Location and Micro-Location

Location remains the single most dominant pricing factor in the UAE, and it operates on multiple levels. At the broadest level, the emirate matters — Dubai commands a significant premium over Sharjah, Ajman, or Ras Al Khaimah, reflecting its infrastructure, liquidity, and global profile. Within Dubai itself, community tier creates dramatic price differences: prime addresses such as Palm Jumeirah, Downtown Dubai, and Emirates Hills sit in an entirely different market from mid-tier communities like Jumeirah Village Circle or Dubai South, which themselves sit above affordable areas like International City or Discovery Gardens.

Beyond community tier, micro-location is critical. A unit facing the Burj Khalifa, a beachfront, a golf course, or the Dubai Creek can command 20 to 40 percent more than a comparable unit facing an internal road or parking structure. Metro proximity, highway access via Sheikh Zayed Road or Emirates Road, and distance to the airport all feed into daily convenience — and buyers price that convenience in.

2. Developer and Project Quality

In the UAE, who built the property matters enormously. Tier-1 developers — Emaar, Aldar, Meraas, Nakheel, and a handful of others — carry a brand premium that typically ranges from 10 to 20 percent above comparable stock from lesser-known or speculative developers. This premium reflects finishing quality, master-planning investment, and critically, delivery track record.

Off-plan projects from developers with a strong handover history price higher because buyers assign lower risk to the timeline and the final product. Conversely, projects from developers with delayed or disputed completions often trade at a discount even when the location and specification are competitive. When evaluating any unit, the developer’s reputation is not a soft factor — it is a quantifiable component of value.

3. Unit-Specific Attributes

Once location and developer are established, the characteristics of the unit itself drive the residual variance in pricing. Built-up area versus plot area matters differently for apartments and villas — for apartments, internal BUA is the primary metric, while for villas, plot size and garden configuration carry significant weight.

Floor level affects pricing in tower projects, with higher floors typically commanding three to eight percent premiums. View is perhaps the most emotionally charged variable: sea, park, skyline, and community views all outperform internal or road-facing orientations. Layout efficiency matters too — a well-designed 1,200 square foot apartment with minimal corridor waste will feel — and price — larger than a poorly planned one of the same area. In the UAE climate, orientation also plays a quiet role, with north-facing units preferred for their reduced heat exposure and east-facing units valued for morning light. Age and condition round out the picture, with newer stock or recently renovated units pricing above aged equivalents in the same building.

4. Community Amenities and Surrounding Infrastructure

Within a development, the quality of shared amenities affects both rental appeal and resale value. Pool quality, gym specification, concierge services, parking ratios, retail within the community, and security standards all contribute to the lifestyle proposition that buyers and tenants are paying for. At the master community level, the developer’s ongoing investment in landscaping, roads, and retail activation separates premium addresses from those that stagnate.

Surrounding infrastructure is equally important for long-term value stability. Proximity to quality schools, hospitals, supermarkets, and restaurants reduces friction for residents and widens the potential buyer and tenant pool. In a desert market, parks and green space command meaningful premiums — particularly for villa communities where outdoor living is a primary draw.

5. Supply and Demand Dynamics

A property does not exist in a vacuum — its value is partly a function of what else is available and what is coming. Upcoming supply pipeline is one of the most underappreciated variables in UAE property analysis. A submarket absorbing 2,000 new units over the next 18 months will price differently from one with limited new delivery, even if current transaction levels look healthy. Jumeirah Village Circle between 2019 and 2021 is a textbook example of oversupply suppressing prices despite strong occupancy numbers.

Absorption rate — how quickly available units are selling — is a useful real-time indicator of market health. Off-plan units are typically priced at a discount to secondary market stock, but this gap narrows as the handover date approaches and the product becomes tangible. Macro-level demand drivers, including population growth, Golden Visa eligibility thresholds, retirement and remote work visa policies, and corporate relocations into the UAE, all feed directly into housing demand and set the underlying floor for pricing.

6. Rental Yield and Investment Return

For investment-oriented buyers — which represents a substantial share of UAE purchasers — the rental yield implied by a given asking price is a fundamental valuation check. Gross yield, calculated as annual rent divided by purchase price, typically ranges from five to eight percent across the UAE market, with higher yields in mid-market areas and lower yields in prime locations where capital appreciation expectations are priced in.

Net yield, after accounting for annual service charges, management fees, and vacancy periods, provides a more realistic picture of income return. Yield compression — where prices rise faster than rents — signals that the market is approaching a ceiling driven by sentiment and liquidity rather than income fundamentals. Tracking the relationship between transaction prices and prevailing rental rates in a given submarket is one of the most reliable tools for identifying overheated conditions before they correct.

7. Legal and Ownership Structure

The legal characteristics of a property have direct pricing implications. Freehold zones, which allow foreign nationals to own property outright, trade at a premium to leasehold areas. A clean title deed, free of mortgage encumbrances and registered with the Dubai Land Department or equivalent authority, is a basic prerequisite for a transparent transaction — any complication here introduces a discount.

Service charges deserve particular attention. A unit carrying an annual service charge of AED 15 per square foot and one at AED 30 per square foot are fundamentally different investment propositions, even at the same purchase price. High service charges erode net yield and suppress buyer appetite at resale. The quality and governance of the Owners Association — its financial reserves, maintenance responsiveness, and compliance with strata law — is a pricing signal that many buyers overlook until they are on the wrong side of a poorly managed building.

8. Macroeconomic and Market Sentiment Factors

The UAE property market is unusually sensitive to global macroeconomic conditions, for several structural reasons. The dirham’s peg to the US dollar means that UAE mortgage rates track the US Federal Reserve’s interest rate decisions closely — a rising rate environment increases the cost of borrowing and reduces purchasing power for mortgage buyers. Oil prices, while less directly correlated than a decade ago, still influence government spending, private sector confidence, and the regional wealth that flows into property.

Exchange rate movements create periodic buying waves. When the British pound, Indian rupee, or Russian ruble weakens significantly against the dollar, UAE property becomes measurably cheaper for buyers from those markets — and transaction volumes from those nationalities tend to spike accordingly. At a broader level, Dubai has established itself as a geopolitical safe-haven asset, and periods of regional instability elsewhere in the Middle East and beyond have consistently driven capital into the market. Transaction volume data from the DLD remains the most reliable ground-truth indicator of genuine market health, as it reflects completed deals rather than listed prices.

9. Valuation Methods Used in Practice

Professional valuers and banks financing UAE property typically apply one or more of the following approaches. The comparable sales method — drawing on DLD transaction data to establish price per square foot benchmarks for similar units in the same area — is the most common and forms the basis of most residential valuations. The income approach, which capitalises net rental income at a market-derived yield rate, is used for investment properties and provides an income-based ceiling on value. The cost approach, estimating land value plus construction cost, is more relevant for new developments. The residual or development approach is applied primarily to land valuations where a developer is pricing a site against its expected development profit.

Data providers including Property Monitor and REIDIN aggregate DLD transactions and provide the comparable evidence base that RERA-certified valuers and bank appraisers use as their primary source.

A Practical Evaluation Framework

When assessing any UAE property, six questions anchor the analysis. What are comparable units actually transacting at — not what they are listed at — on a per square foot basis? What gross yield does the asking price imply, and how does that compare to the submarket average? What is the annual service charge per square foot, and what does the OA’s financial position look like? What new supply is entering this submarket over the next 12 to 24 months? Is the developer Tier 1, and what is their delivery track record? And finally, what is the exit liquidity — how quickly and at what discount could this unit be resold if required?

Together, these questions move a property evaluation from gut instinct to structured analysis — which is the standard any serious buyer, investor, or advisor should be working to.